The Challenge of Anesthesia Contracting

Summary:

While reasonable payment rates among commercial plans for anesthesia services were forthcoming in the past, it is clearly becoming more difficult to obtain adequate rates from many payers. This, coupled with fairly flat Medicare and Medicaid rates and a growing Medicare and Medicaid population, translates to significant pressure on group revenue.

The traditional view of effective practice management considered aggressive payer contracting essential to optimizing practice finances. Conventional wisdom has always held that it is easier to get money from insurance plans than from patients. The problem is that public payer rates for Medicare, Medicaid and workers compensation are non-negotiable. This has meant that anesthesia practices have had to focus their negotiations on an ever-shrinking percentage of commercial payers such as the Blues, Aetna, Cigna and United.

It used to be that most practices could offset low public payer rates with aggressive commercial rates, and it was not uncommon for commercial contract rates to be three or four times the Medicare rate. The sad truth is that this strategy seems to be losing momentum. A ten-year review of contract rates clearly indicates that most commercial insurance plans are starting to push back and limit annual increases in their contract rates, and the ultimate impact of the COVID-19 pandemic was to force most payers into a permanent holding pattern with regard to granting any rate increases.

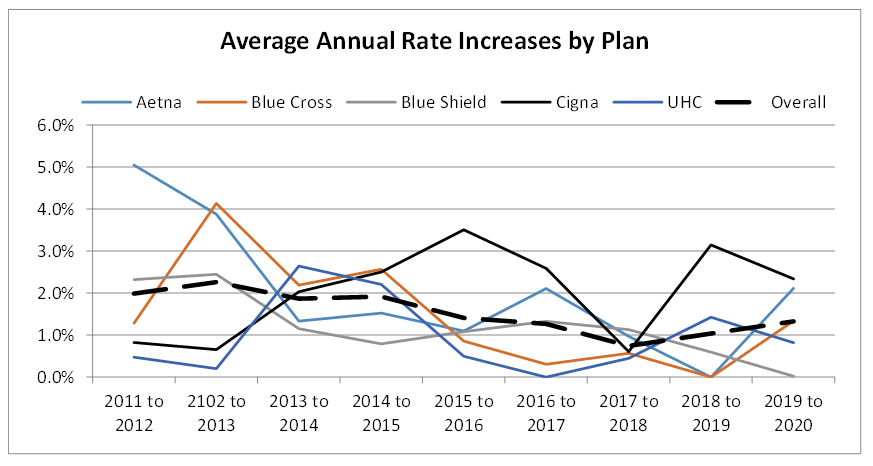

The focus of our review was five payer plans for 20 client practices with ten years of accounts receivable data. We limited our analysis to contract rates and actual payments for surgical cases, as distinct from obstetric cases and non-time-based services such as invasive monitoring, nerve blocks, guidance changes and visits. It should be noted that while many states only have Blue Shield plans, California, Oregon, Idaho and Pennsylvania also have Blue Cross plans administered by Anthem.

There was a time when a practice would renegotiate its rate with a plan for a period of three to five years at a specific rate. Then it became common for contracts to include a small escalator from one year to the next. Such contracts tend to limit the subsequent year rate increases. As the chart below indicates, while some clients in some locations have been able to negotiate two and three percent annual rate increases in the early part of the decade with the exception of CIGNA and United Healthcare, the overall trend is downward. Blue Cross of California, for example, has not been willing to give rate increases for the past few years.

The slight increase in the average contract rate from 2018 to 2020 (0.7 to 1.3 percent) may represent a little light at the end of the tunnel and be an acknowledgement that the cost of anesthesia services continues to rise. The reality is that Medicare rates have remained pretty flat while the percentage of Medicare patients has continued to increase by about one percent per year for this entire period. This inability to cost shift explains why hospital subsidy negotiations have become so critical to practice survival. For most practices it has simply become impossible to cover the cost of payroll with professional fee income.

Unfortunately, this is not the end of the story. Commercial insurance plans always involve a deductible and a co-payment, usually 20 percent of the allowable. Although patient willingness and ability to pay their share of medical bills has been declining, the impact of the COVID-19 pandemic was particularly significant. What this means is that minimal rate increases are actually offset by declining collections.

Just to put this in perspective, if an average Blue Shield allowable was $500 and the plan paid 80 percent, then the insurance payment was $400. In 2011, the average patient paid 75 percent or $75 for a total payment of $475, which meant the practice collected 95 percent of the allowable. By 2020, however, the average percentage dropped to 62 percent meaning the patient only paid $62, thus resulting in a total payment of $462 or 92.5 percent of the allowable. Even if the rate had gone up by one percent, the net payment to the practice dropped by more than one percent.

This data represents a compelling reason to push harder on payers so that the net effect of contract rate increases is positive. Due to this, we renegotiate managed care contracts on an annual basis and include patient co-pays and deductibles in these discussions. The real take-away here is that, as revenue potential continues to decline, the most important priority of all practices must be cost management. If you have any questions in regards to your contract rates, please contact your account executive or email us at info@anesthesiallc.com for a detailed review.